Investment in Your Child’s Future – Mutual Fund SIP for Your Little One

Hi parents!!

I am the father of a princess who’s 1 year 1 month old. Just a few months ago I was just calculating the number of useless expenses which I had been doing. Sometimes buying an iPhone, or the latest watch, etc.

To my surprise when I did a calculation of all the expenses since I started earning, it was more than 5-7 lakhs in 5 yrs.

The expense of nurturing the baby could be challenging and so I urge all the parents to take this step of investing in a children mutual fund by the means of SIP.

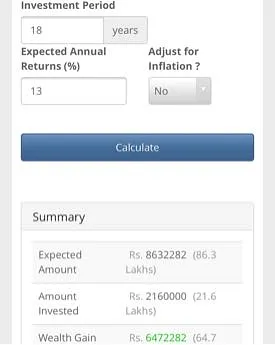

1) I have taken a “Children’s Mutual Fund” and have been putting Rs 10,000/- every month as SIP.

You can invest the funds as per your affordability.

I have sworn never to touch this fund until my daughter is atleast 18 years old.

Considering a min rate of interest as 13% which this fund will give me. The returns when she’ll turn 18 years old will be 86 lakhs.

Yes with just an investment of around 21 lakhs over 18 years, you will get 86 lakhs in return.

That’s the power of compounding interest.

2) There is also another beautiful investment scheme by the Government and it is called “Sukanya Scheme”. But its only for girl children.

This gives an average return rate of around 9% and you can put a maximum of 1 lakh per year.

The best part is you can even get a tax benefit if you invest in this scheme.

The only downside( or you can say upside) is that you cannot withdraw the amount from this account till the girl is 18 years old.

Also, the amount can be redeemed only for her education or marriage expenses pre-maturity.

I don’t have much information on Sukanya scheme as i have just opened it for namesake, however, you can Google it if you want more details on it.

Start today for the future of your little one.

Disclaimer: The views, opinions and positions (including content in any form) expressed within this post are those of the author alone. The accuracy, completeness and validity of any statements made within this article are not guaranteed. We accept no liability for any errors, omissions or representations. The responsibility for intellectual property rights of this content rests with the author and any liability with regards to infringement of intellectual property rights remains with him/her.

Was This Article Helpful?

Parenting is a huge responsibility, for you as a caregiver, but also for us as a parenting content platform. We understand that and take our responsibility of creating credible content seriously. FirstCry Parenting articles are written and published only after extensive research using factually sound references to deliver quality content that is accurate, validated by experts, and completely reliable. To understand how we go about creating content that is credible, read our editorial policy here.

- Author

")

")

")